Over the last six months, RLI’s shares have sunk to $65.35, producing a disappointing 14.2% loss - a stark contrast to the S&P 500’s 22.7% gain. This might have investors contemplating their next move.

Following the drawdown, is now an opportune time to buy RLI? Find out in our full research report, it’s free for active Edge members.

Why Does RLI Spark Debate?

Founded in 1965 and named after its original focus on "replacement lens insurance" for contact lens wearers, RLI (NYSE:RLI) is a specialty insurance company that underwrites property, casualty, and surety products through wholesale brokers, independent agents, and carrier partnerships.

Two Positive Attributes:

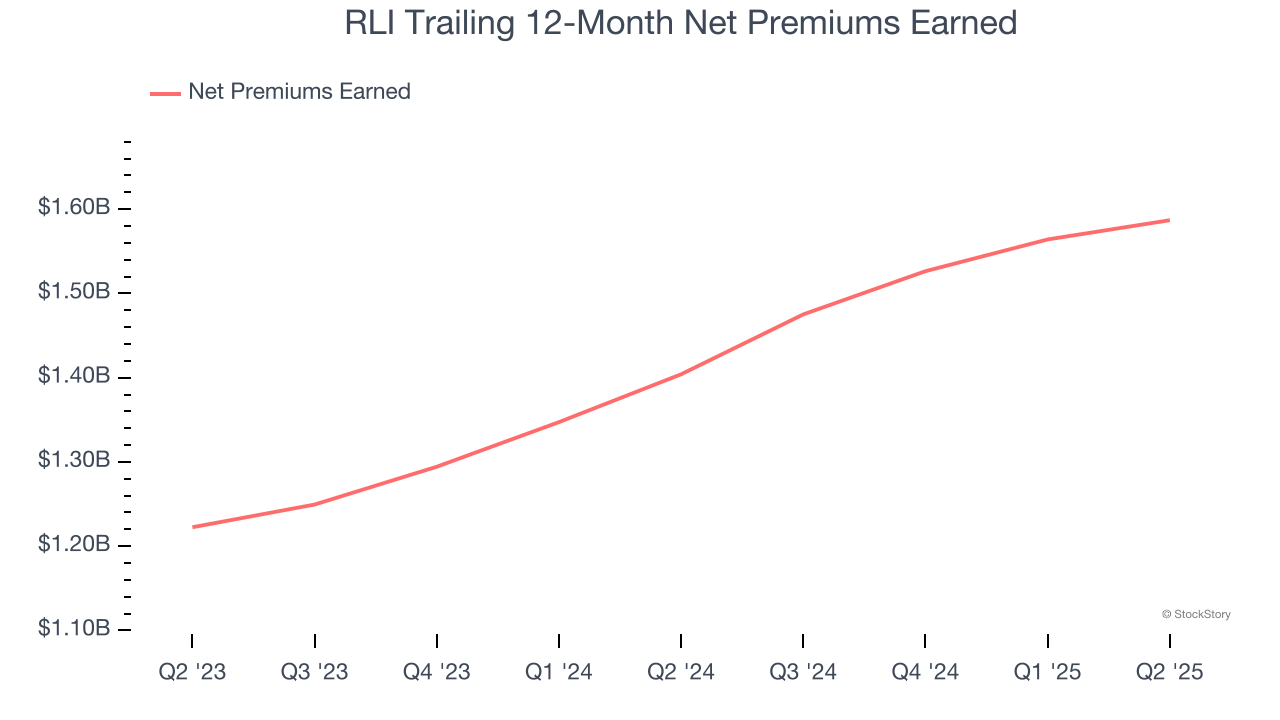

1. Net Premiums Earned Skyrocket, Fueling Growth Opportunities

Net premiums earned are net of what’s paid to reinsurers (insurance for insurance companies), which are used by insurers to protect themselves from large losses.

RLI’s net premiums earned has grown at a 13.9% annualized rate over the last two years, much better than the broader insurance industry and faster than its total revenue.

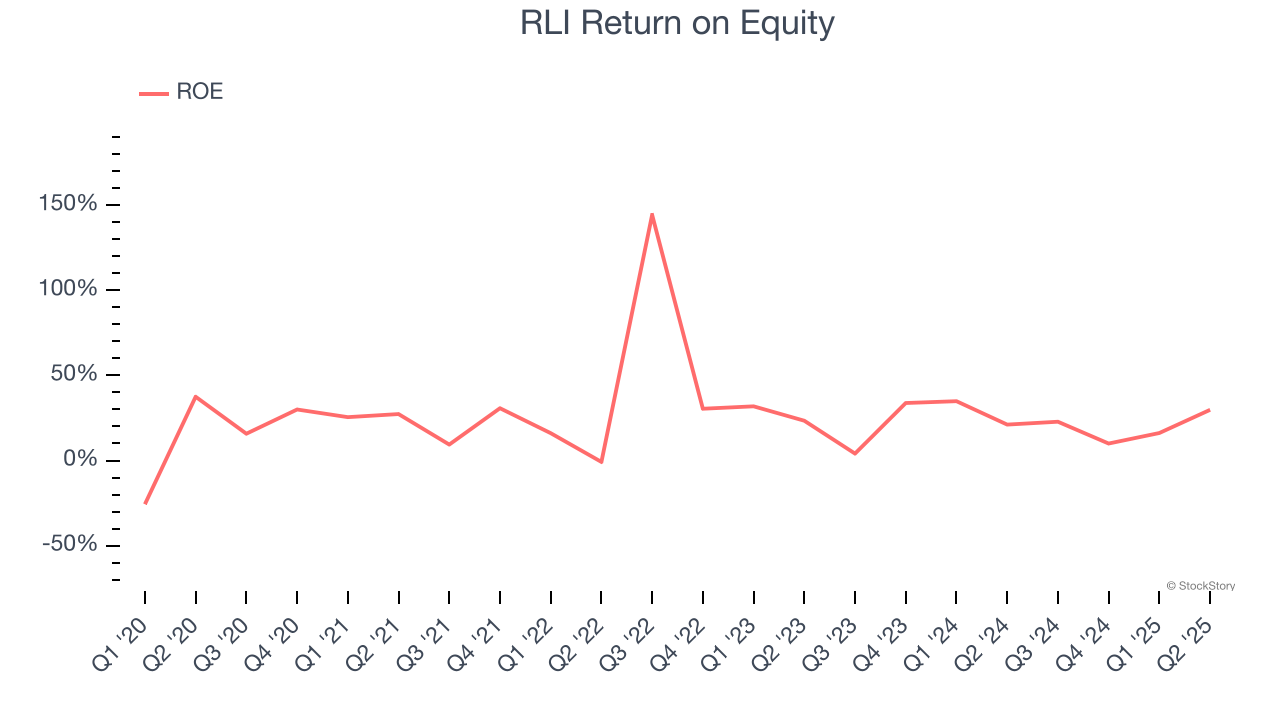

2. Stellar ROE Showcases Lucrative Growth Opportunities

Return on Equity, or ROE, ties everything together and is a vital metric. It tells us how much profit the insurer generates for each dollar of shareholder equity entrusted to management. Over a long period, insurers with higher ROEs tend to compound shareholder wealth faster through retained earnings, buybacks, and dividends.

Over the last five years, RLI has averaged an ROE of 27.8%, exceptional for a company operating in a sector where the average shakes out around 12.5% and those putting up 20%+ are greatly admired. This shows RLI has a strong competitive moat.

One Reason to be Careful:

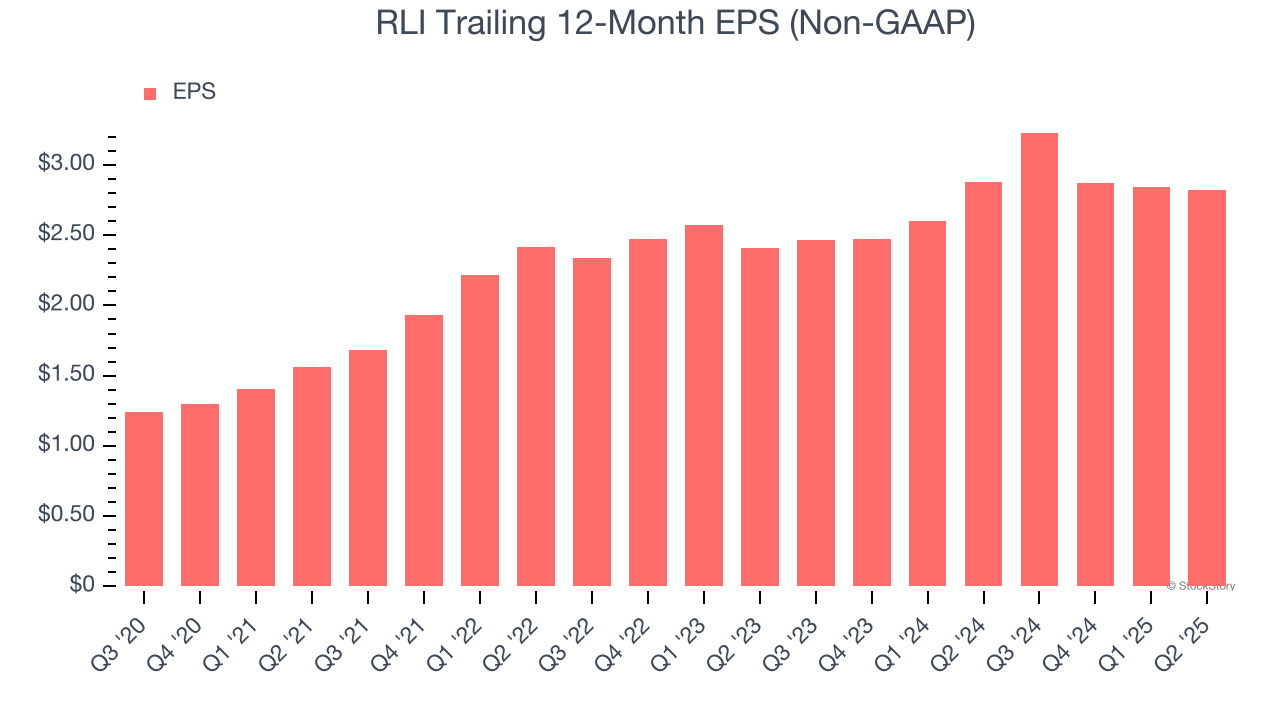

Recent EPS Growth Below Our Standards

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

RLI’s EPS grew at a weak 8.3% compounded annual growth rate over the last two years, lower than its 10.3% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

RLI’s merits more than compensate for its flaws. After the recent drawdown, the stock trades at 3.5× forward P/B (or $65.35 per share). Is now the time to initiate a position? See for yourself in our in-depth research report, it’s free for active Edge members.

High-Quality Stocks for All Market Conditions

Donald Trump’s April 2025 "Liberation Day" tariffs sent markets into a tailspin, but stocks have since rebounded strongly, proving that knee-jerk reactions often create the best buying opportunities.

The smart money is already positioning for the next leg up. Don’t miss out on the recovery - check out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.